An EU country's tax administration has decided that a Latvian holding company is not a UBO for dividends it receives, so it has to look through. Let me explain this as many now go into export markets.

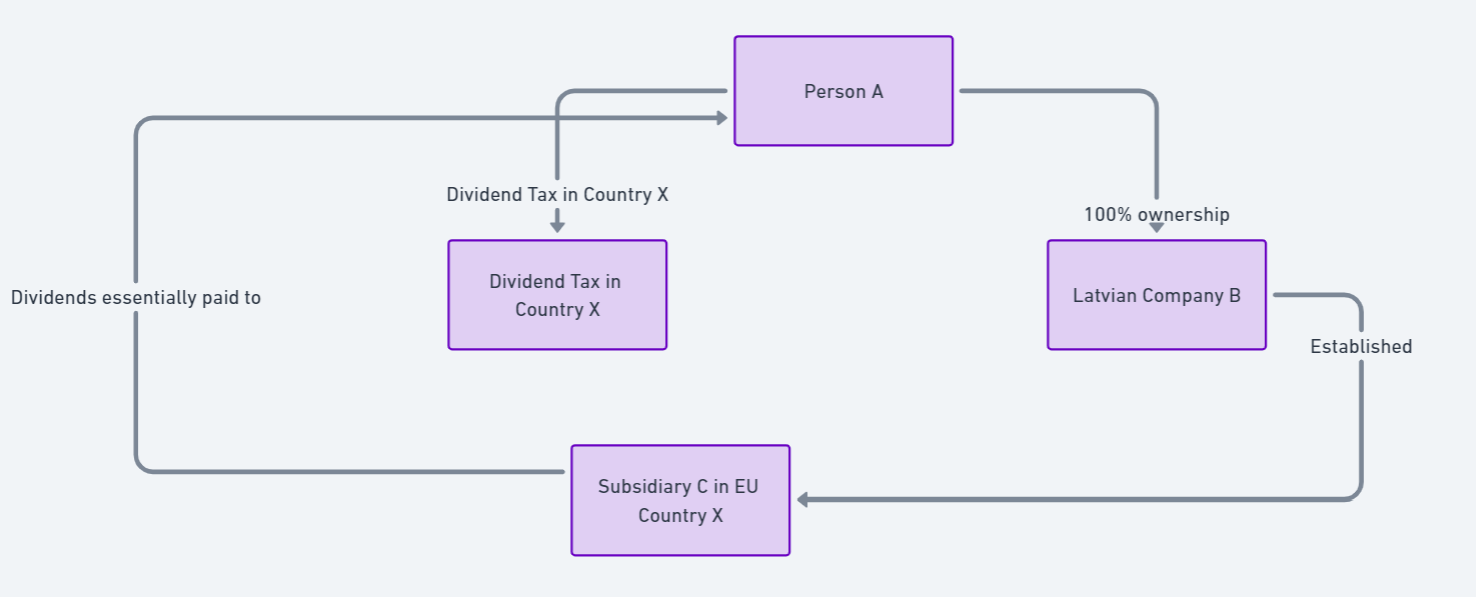

In the situation A-B-C, C must be considered paying to A

{kind=link}

A person A, resident in Latvia, owns 100% shares in a Latvian limited liability company B. B, in turn, has established a subsidiary C in the EU country X. The administration in country X said that it considered that the dividends were in substance paid by C to A directly, and not to B. If dividends are paid out of X to an individual in Latvia, then the dividend is subject to a withholding tax in country X.

LatviaFrom a Latvian perspective, if company C has paid CIT in an EU country (and of course it has paid CIT in country X), then neither CIT nor PIT is payable in Latvia on dividends received from company C. Therefore, the administration in country X claims that B was created in Latvia only for tax saving purposes. Therefore, B may be disregarded for tax purposes in country X.

How is this justified?Then a rather complicated exercise begins. You have to look at the national laws and case law in country X, the relevant tax convention, in combination with the EU's so called "Parent-Subsidiary Directive" and the judgments of the EU Court of Justice. An undesirable situation, regardless of who is right.

Beneficial ownershipPart of the problem comes from the tax treaty which allows a reduced withholding tax rate on dividends if the recipient is the beneficial owner of the dividend. This means that the recipient is not a letterbox company that does nothing and passes on the dividends received. This is why the so-called UBO test (beneficial ownership), which I have written about at some length above, applies worldwide. There I also described 6 important criteria established by the EU Court of Justice which can be indicative of an artificial holding structure. By the way, Tax Stories podcast guest Błażej Kuźniacki has written a whole book on this BO principle.

But...In this situation, the tax treaty will not apply at all, because we do not want to apply the reduced withholding tax rate of the treaty, but the exemption from this tax. Therefore, the national law of the relevant EU country (X) and its interpretation of the relevant EU directive, which prohibits the application of CIT to dividends within the EU territory, will apply. Moreover, one should check that the national law of country X complies with the principles set out in the EU Directive and the case law of the EU Court of Justice.

Treaty shoppingMost of the high-profile judgments of the CJEU have involved the well-known jargon in tax circles - treaty shopping. This means that a company is set up in a country because it has a more favourable tax treaty regime. But such artificial box-ticking has long been unheard of in the modern world. Also in the case of country X above, there is no treaty shopping because A and B are located in the same country.

Therefore, any corporate structure must now critically assess the economic substance of their holding company and whether anyone in the country of business can say that the holding is set up to gain tax advantages.