Now’s a great time to buy property. Here’s why…

Investopoly

English - July 26, 2022 21:00 - 16 minutes - 11.3 MB - ★ - 1 ratingInvesting Business investing financial advice property shares tax borrowing wealth retirement super Homepage Download Apple Podcasts Google Podcasts Overcast Castro Pocket Casts RSS feed

In mid-2021, I wrote this blog: “Don’t buy a property in this market…” because, at that time, many property buyers were over-paying for property just to get into the market. I call it the FOMO premium, for lack of a better term (more about this below). My thesis was that since it’s never wise to allow fear (e.g., FOMO) to influence financial decision making, it was better to not buy property in 2021 if it meant having to overpay.

We all know that the market has cooled somewhat this year. It is now my view that this is a much better market to buy in, if you can find the right asset, of course.

What drove the property boom in 2020 and 2021?

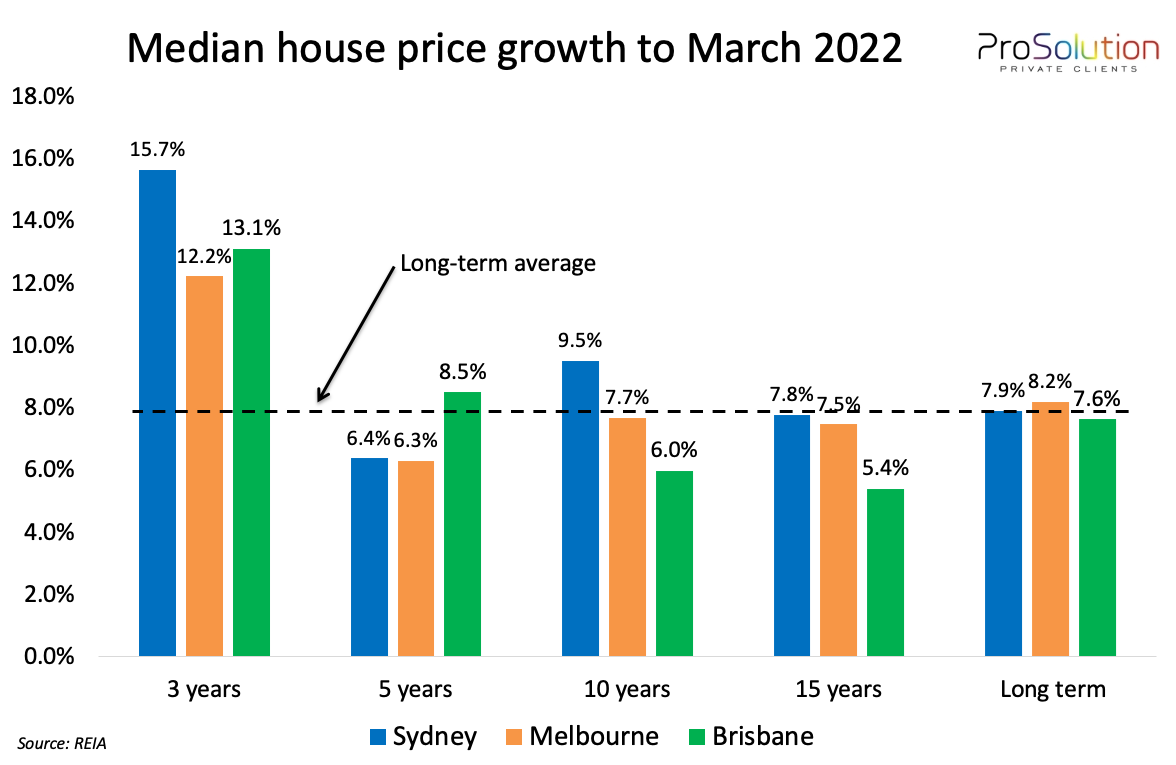

The median house price in the eastern capital cities grew by between 12% and 16% p.a. compounding over the 3 years ended March 2021. I believe this growth was driven by two predominant factors:

1. Long-horizon mean reversion; and

2. FOMO premium.

The market was mostly making up for lost ground

The chart below illustrates the historic compounding capital growth of the median house price in Melbourne, Sydney and Brisbane for the periods ending March 2022. The “long-term” figures reflect growth over the past 42 years i.e., 1980 to 2022.

{kind=link}

Whilst recent growth in property prices was well above the long-term average and therefore unsustainable, longer-term growth rates are still below the long-term averages with only two exceptions:

1. Sydney’s growth rate over the past 10 years exceeds the long-term average by 1.60% p.a. However, growth over 15 years is in line with the long-term average. Therefore, it’s possible that Sydney prices have over-corrected over recent years and could enter into a flatter cycle for the few years; and

2. Brisbane’s growth rate over the past 5 years has exceeded its long-term average. It is noteworthy however that growth over 10 and 15 years is still below average, so this market is probably still undervalued and could continue to grow strongly to revert to its mean.

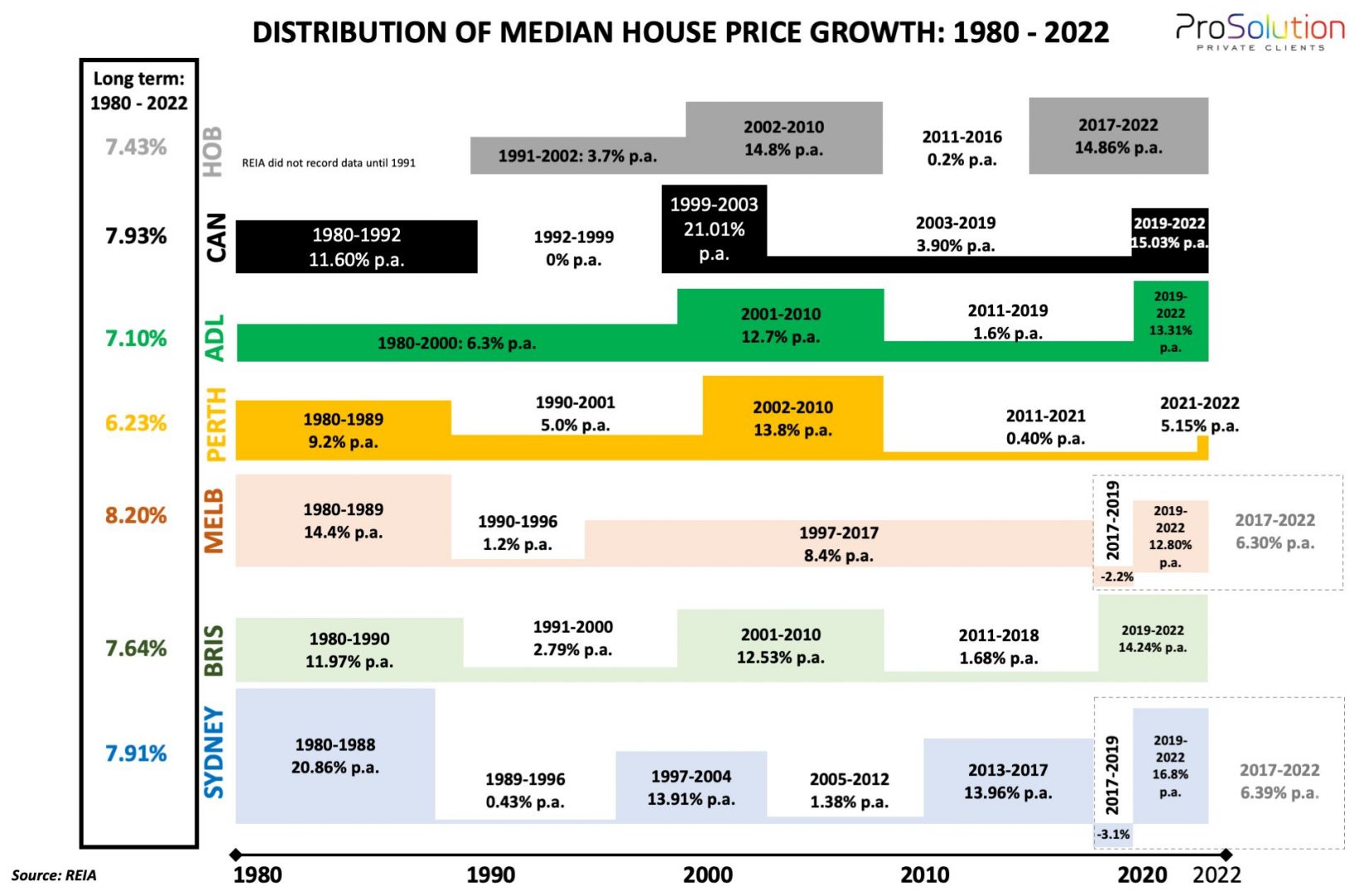

This updated chart demonstrates that property markets tend to move in two distinct cycles: a flat cycle followed by a growth cycle. To a large extent, this is what happened in Melbourne and Sydney after posting house price declines over the 3 years prior to the beginning of Covid. As demonstrated, the 5-year growth is still below average.

{kind=link}

The FOMO premium

Australia’s reaction to Covid throughout 2020 and 2021 fueled demand for property:

§ The cash rate was ostensibly cut to zero. The RBA lent cheap money to the banks which they used to fund very low fixed rate loans, often at rates below 2% p.a.

§ Higher income earners were able to preserve their incomes because their occupations were able to be conducted from home, unlike lower-income earners that worked in retail, hospitality and travel, for example.

§ Due to the lockdowns, higher-income-earners spent less and saved more – they enjoyed much larger levels of surplus cash flow.

§ And finally, people were spending more time at home which invited them to reflect on whether their home adequately suited their lifestyle needs.

These factors conspired to create a lot of demand for property, particularly from higher income earners who considered upgrading their home (i.e., demand was mainly fueled by owner-occupiers, not investors).

In early 2021, the co