Don't underestimate the mathematical power of gearing

Investopoly

English - April 20, 2021 23:00 - 15 minutes - 10.6 MB - ★ - 1 ratingInvesting Business investing financial advice property shares tax borrowing wealth retirement super Homepage Download Apple Podcasts Google Podcasts Overcast Castro Pocket Casts RSS feed

It’s stating the obvious to say interest rates are very low at the moment. But what can be easily missed is how powerful low rates can be for investors. And arguably, the next few decades could provide the best opportunities in a lifetime for investors, if they are diligent and invest in high quality assets.

When will interest rates rise?That is the million-dollar question. The short answer is that no one really knows. But we should remind ourselves that interest rate expectations can change very quickly, so we must factor that into our investment decision making. That is, make sure you can afford higher loan repayments when rates eventually rise.

The RBA has been very firm in regard to its intention. It has said that it will not raise rates until the inflation rate rises above 2% p.a., which it does not expect will occur before 2024. Therefore, it seems variable rates are on hold for at least 2.5 more years.

We should consider the level of government indebtedness and the impact rising interest rates will have on the budget. Economies can become reliant on low interested rates – look at Japan as an example. It has been stuck on zero interest rates for more than 20 years.

For what it’s worth, my view is that variable rates probably won’t change materially over the next 3 to 5 years. Beyond 5 years, they are likely to rise but probably at a relatively slow pace. It is quite difficult to fathom rates rising above 5-6% p.a. over the next few decades. Low rates could be the “new normal”.

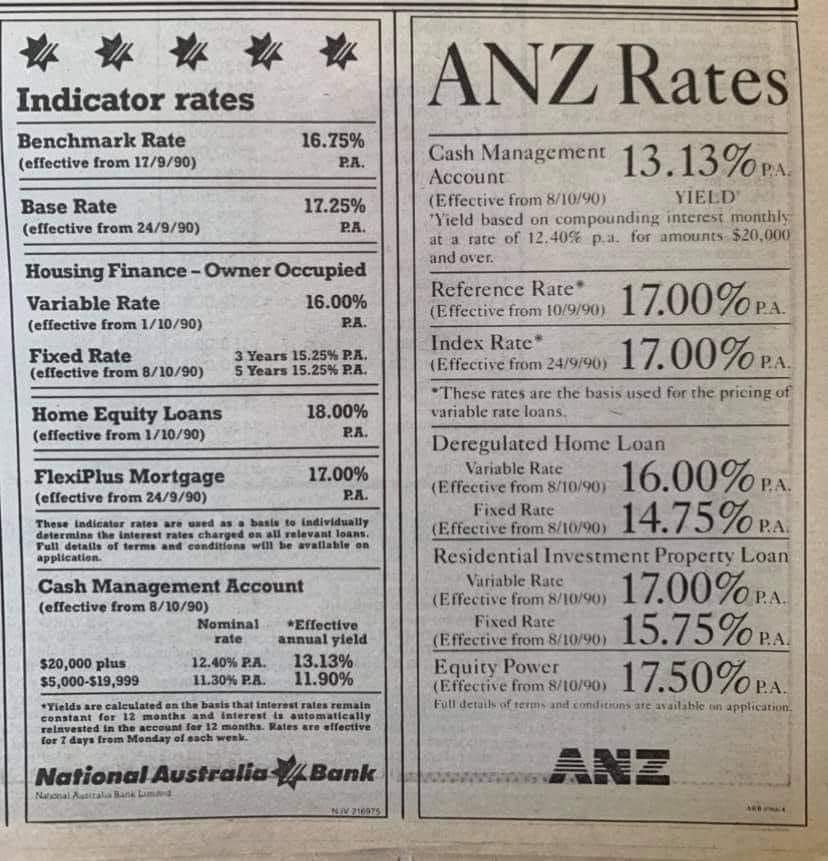

Simple math proves its powerInvestors can lock in an interest rate for 5 years at 2.69% p.a. with interest-only repayments. I think we can all agree that is low (especially compared to early 1990’s rates, as shown in this image doing the rounds on social media).

Assuming you have a surplus annual cash flow of $25,000 to invest, you have two obvious options:1. Invest it incrementally each year in an investment such as a share market index fund; or2. Borrow a lump sum, buy an investment property and use the cash flow to pay for its net holding costs.

If you chose the first option and you received a return of 10% p.a. over the next 20 years (wh

{kind=link}

ASK ME A QUESTION ON YOUTUBE: https://www.youtube.com/watch?v=ACnxmEP8vv8

My YouTube channel: https://youtube.com/@investopolypodcast

If this episode resonated with you, please leave a rating on your favourite podcast platform. It helps me reach more incredible listeners like you. Thank you for being a part of this journey! :-)

Click here to subscribe to Stuart's weekly email.

SPECIAL OFFER: Buy a one of Stuart's books for ONLY $20 including delivery. Use the discount code blog here.

Work with Stuart's team: At ProSolution Private Clients we encourage clients to adopt a holistic and evidence-based approach when making financial decisions. Visit our website.

IMPORTANT: This podcast provides general information about finance, taxes, and credit. This means that the content does not consider your specific objectives, financial situation, or needs. It is crucial for you to assess whether the information is suitable for your circumstances before taking any actions based on it. If you find yourself uncertain about the relevance or your specific needs, it is advisable to seek advice from a licensed and trustworthy professional.